Bank Reconciliation Statement Definition

Bank Reconciliation: To do a bank rapprochement you would match the cash harmonies on the balance sheet to the comparable amount on your bank statement, determining the differences between the two in order to make developments to the accounting records, resolve any discrepancies and identify fraudulent negotiations.

Did you know? To make the topic of Bank Rapprochement even easier to find out, we created a collection of premium materials called PRO. Our PRO users get career access to our bank rapprochement visual tutorial, cheat sheet, flashcards, quick tests, a quick test with coaching, business forms, and more.

Bank Reconciliation Template

In bookkeeping, bank reconciliation is the process by which the bank account balance in an entity’s books of account is reconciled to the balance as reported by the financial institution in a bank statement. If there is a difference in the two figures as at a specified date the difference needs to be explained and rectified.

Bank statements are commonly routinely produced to enable account holders to perform bank reconciliations.

Such differences may occur, for example, because:

- cheques issued by the organization that has not been presented to the bank,

- a banking transaction, such as credit received, or a charge made by the bank, has not yet been recorded in the organization’s books, or

- either the bank or the organization itself has made an error.

Sometimes it may be easy to accommodate the difference by looking at the transactions in the bank announcement since the last rapprochement and the organization’s own accounting records (cash book) to see if some combination of them tally with the characteristic to be explained. Otherwise, it may be necessary to go through and match every transaction in both sets of records since the last rapprochement and see what transactions remain unmatched. The unavoidable adjustments should then be made in the cash book or disclosed to the bank if necessary, or any timing arguments recorded to assist with future rapprochement.

For this reason, and to minimize the amount of work involved, it is good practice to carry out such reconciliations at intelligently frequent intervals. rapprochement may be assisted by specialized accounting software. Many financial institutions now offer direct downloads of financial instruction into account holders’ accounting software to streamline the reconciliation process.

Bank Reconciliation Example

A company’s commonplace ledger account Cash incorporates a record of the transactions (checks are written, receipts from customers, etc.) that involve its checking account. The bank also organizes a record of the company’s checking account when it handles the company’s checks, securities, service charges, and other items. Soon after each generation ends the bank usually mails a bank statement to the company. The bank statement lists the activity in the bank account during the recent month as well as the tension in the bank account.

When the company receives its bank announcement, the company should verify that the amounts on the bank statement are consistent or adaptable with the amounts in the company’s Cash account in its general ledger and vice versa. This process of confirming the amounts is transferred to as reconciling the bank statement, bank statement reconciliation, bank reconciliation, or doing a “bank rec.” The benefit of reconciling the bank statement is knowing that the amount of Cash reported by the company (company’s books) is consistent with the amount of cash shown in the bank’s records.

Because most companies write hundreds of checks each month and make many deposits, reconciling the amounts on the company’s books with the amounts on the bank statement can be time-consuming. The process is complicated because some items appear in the company’s Cash account in one month but appear on the bank statement in a different month. For example, checks written near the end of August are deducted immediately on the company’s books, but those checks will likely clear the bank account in early September. Sometimes the bank decreases the company’s bank account without informing the company of the amount. For example, a bank service charge might be deducted on the bank statement on August 31, but the company will not learn of the amount until the company receives the bank statement in early September. From these two examples, you can understand why there will likely be a difference in the balance on the bank statement vs. the balance in the Cash account on the company’s books. It is also possible (perhaps likely) that neither balance is the true balance. Both balances may need adjustment in order to report the true amount of cash.

After you adjust the balance per bank to be the true balance and after you adjust the balance per books to also be the same true balance, you have reconciled the bank statement. Most accountants would simply say that you have done the bank reconciliation or the bank rec.

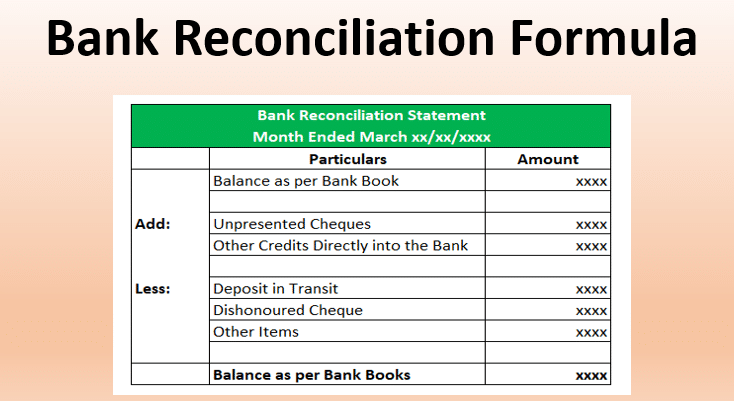

Bank Reconciliation Statement

A bank reconciliation statement is a document that matches the cash balance on a company’s balance sheet to the corresponding amount on its bank statement. Reconciling the two accounts helps determine if accounting changes are needed. Bank reconciliations are completed at regular intervals to ensure that the company’s cash records are correct. They also help detect fraud and any cash manipulations.

When banks send companies a bank statement that contains the company’s beginning cash balance, transactions during the period, and ending cash balance, almost always the bank’s ending cash balance and the company’s ending cash balance are not the same. Some reasons for the difference are:

- Deposits in transit: Cash and checks that have been received and recorded by the company but have not yet been recorded on the bank statement.

- Outstanding checks: Checks that have been issued by the company to creditors but the payments have not yet been processed.

- Bank service fees: Banks deduct charges for services they provide to customers but these amounts are usually relatively small.

- Interest income: Banks pay interest on some bank accounts.

- Not sufficient funds (NSF) checks: When a customer deposits a check into an account but the account of the issuer of the check has an insufficient amount to pay the check, the bank deducts from the customer’s account the check that was previously credited. The check is then returned to the depositor as an NSF check.

Nowadays, many companies use specialized accounting software in bank reconciliation to reduce the amount of work and adjustments required and to enable real-time updates.

A Bank Reconciliation Should Be Prepared

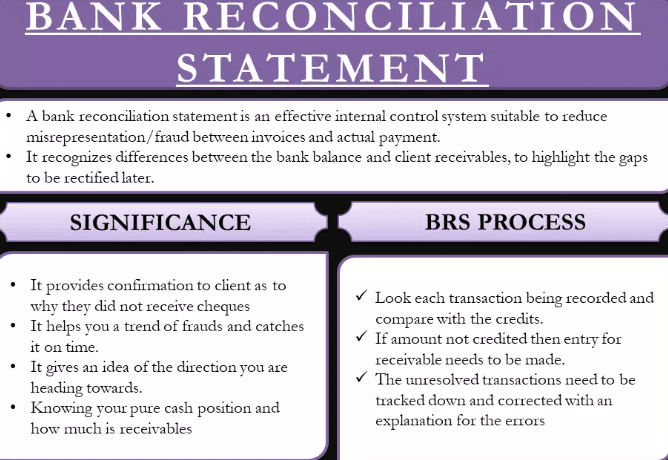

A bank reconciliation statement is a summary of banking and business activity that reconciles an entity’s bank account with its financial records. The statement outlines the deposits, withdrawals, and other activities affecting a bank account for a specific period. A bank reconciliation statement is a useful financial internal control tool used to thwart fraud.

Bank reconciliation statements ensure payments have been processed and cash collections have been deposited into the bank. The reconciliation statement helps identify differences between the bank balance and book balance, in order to process necessary adjustments or corrections. An accountant typically processes reconciliation statements once a month.

- A bank reconciliation statement summarizes banking and business activity, reconciling an entity’s bank account with its financial records.

- Bank reconciliation statements confirm that payments have been processed and cash collections have been deposited into a bank account.

- All fees charged on an account by a bank must be accounted for on a reconciliation statement.

- After all adjustments, the balance on a bank reconciliation statement should equal the ending balance of the bank account.

Completing a bank reconciliation statement requires using both the current and the previous month’s statements, including the closing balance of the account. The accountant typically prepares the bank reconciliation statement using all transactions through the previous day, as transactions may still be occurring on the actual statement date.

All deposits and withdrawals posted to an account must be used to prepare a reconciliation statement

The accountant adjusts the ending balance of the bank statement to reflect outstanding checks or withdrawals. These are transactions in which payment is en route but the cash has not yet been accepted by the recipient. An example is a check mailed on Oct. 30. When preparing the Oct. 31 bank reconciliation statement, the check mailed the previous day is unlikely to have been cashed, so the accountant deducts the amount from the bank balance. There may also be collected payments that have not yet been processed by the bank, which requires a positive adjustment.

What is the journal entry for bank reconciliation?

Journal entries are required in a bank reconciliation when there are adjustments to the balance per books. These adjustments result from items appearing on the bank statement that have not been recorded in the company’s general ledger accounts.

What is a bank reconciliation statement with an example?

A cheque of $300 was deposited, but not collected by the bank. Bank charges of $50 were recorded in Passbook, but not in Cash Book. Cheques worth $200 were issued, but not presented for payment. Bank interest of $100 was recorded in Passbook, but not in Cash Book.