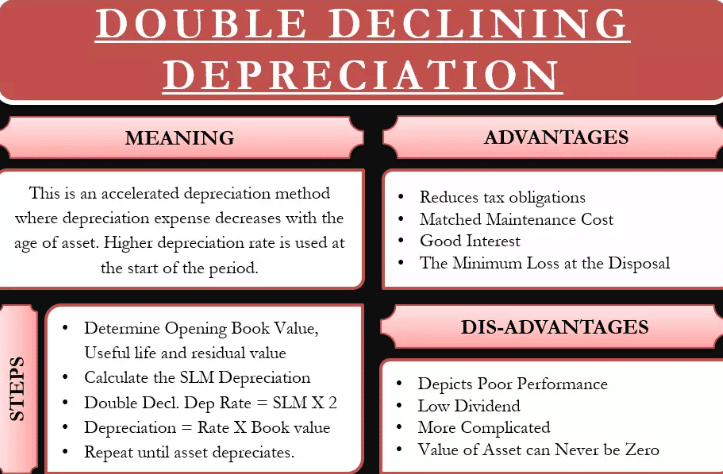

Double Declining Balance Method: The double declining harmony method of reduction, also known as the 200% declining balance method of depreciation, is a form of an increased depreciation. This means that correlated to the straight-line method, the depreciation investment will be faster in the early years of the asset’s life but slower in the later years. However, the total amount of reduction expenses during the life of the assets will be the same.

The “double” means 200% of the straight-line rate of depreciation, while the “declining balance” refers to the asset’s book value or carrying meaning at the beginning of the bookkeeping period. Since book value is an asset’s cost minus its compiled depreciation, the asset’s book profit will be decreasing when the contra asset interest Accumulated Depreciation is credited with the reduction expense of the accounting period.

The double-declining balance depreciation method is a form of accelerated depreciation that doubles the regular depreciation approach. It is frequently used to depreciate fixed assets more heavily in the early years, which allows the company to defer income taxes to later years. This guide will explain how it works and provide examples.

Double Declining Balance

The double-declining tension method is an increased form of the reduction under which most of the reduction associated with a fixed asset is recognized during the first few years of its useful life. This approach is plausible under either of the following two precedences:

- When the utility of an asset is being exhausted at a more rapid rate during the early component of its useful life;

- when the intent is to recognize more investment now, thereby shifting profit perception further into the future (which may be of use for suspending income taxes).

However, this practice is more difficult to calculate than the more conventional straight-line method of depreciation. Also, most benefits are utilized at a tenacious rate over their useful lives, which does not reflect the rapid rate of depreciation resulting from this method. Further, this access results in the skewing of profitability result in future periods, which makes it more troublesome to ascertain the true practical profitability of asset-intensive businesses.

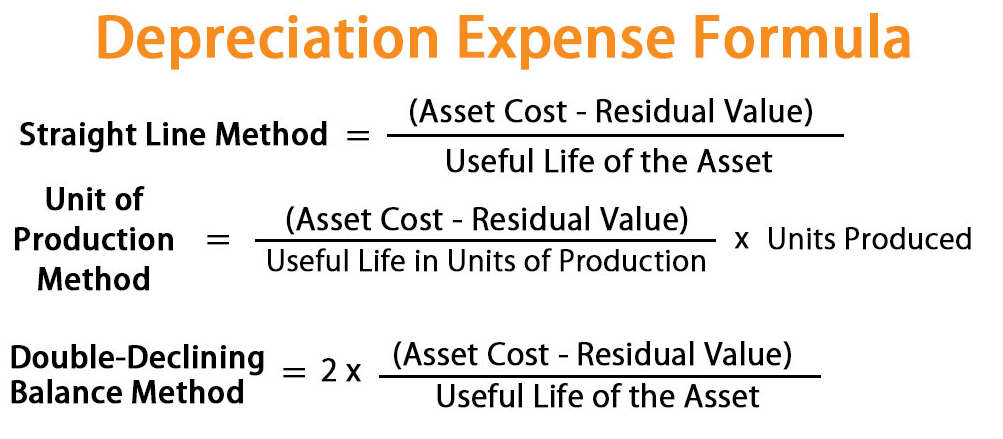

To calculate depreciation under the double-declining method, multiply the asset book value at the beginning of the fiscal year by a multiple of the straight-line rate of depreciation. The double-declining balance formula is:

Double-declining balance (ceases when the book value = the estimated salvage value)

2 × Straight-line depreciation rate × Book value at the beginning of the year

A variation on this method is the 150% declining balance method, which substitutes 1.5 for the 2.0 figure used in the calculation. The 150% method does not result in as rapid a rate of depreciation at the double-declining method.

Example of Double Declining Balance Depreciation

ABC Company purchases a machine for $100,000. It has an estimated salvage value of $10,000 and a useful life of five years. The double-declining balance depreciation calculation is:

|

Year |

Netbook value, |

Double-declining balance depreciation computed as 2 × SL rate × beginning NBV |

Netbook value, |

|

| 1 | $100,000 | $40,000 | $60,000 | |

| 2 | 60,000 | 24,000 | 36,000 | |

| 3 | 36,000 | 14,400 | 21,600 | |

| 4 | 21,600 | 8,640 | 12,960 | |

| 5 | 12,960 | 2,960 | 10,000 | |

| Total | $90,000 |

Double Declining Balance Formula

A double-declining harmony method is a form of an increased depreciation method in which the asset value is depreciated at twice the rate it is done in the straight-line method. Since the depreciation is done at a faster rate (twice to be precise) of the straight-line method it is called increased reduction.

The double-declining balance method is an increased depreciation method. Using this practice the Book Value at the introduction of each period is multiplied by a fixed Depreciation Rate which is 200% of the straight line slump rate, or a factor of 2. To calculate depreciation based on a different factor use our Declining Tension Calculator.

The double-declining harmony calculation does not consider the salvage value in the depreciation of each period however if the book value will fall below the salvage value, the last term might be accommodated so that it ends at the salvage value. When the double-declining balance method does not fully depress an asset by the end of its life, variable receding balance practice might be used instead.

- Straight-Line Depreciation Percent = 100% / Useful Life

- Depreciation Rate = 2 x Straight-Line Depreciation Percent

- Depreciation for a Period = Depreciation Rate x Book Value at Beginning of the Period

- If the first year is not a full 12 months and is a number M months, the first and last years will be calculated

- First-Year Depreciation Rate = M/12 x Depreciation Rate

- Last Year Depreciation Rate = (12-M)/12 x Depreciation Rate

However, accelerated depreciation does not mean that the depreciation expense will also be higher.

Double Declining Balance Calculator

Double declining balance depreciation isn’t a tongue twister invented by bored IRS employees—it’s a smart way to save money upfront on business expenses.

With the double-declining balance method, you depreciate less and less of an asset’s value over time. That means you get the biggest tax write-offs in the years right after you’ve purchased vehicles, equipment, tools, real estate, or anything else your business needs to run.

Depreciation is the act of writing off an asset’s value over multiple tax years and reporting it on IRS Form 4562. The double-declining balance method of depreciation is just one way of doing that. Double declining balance is sometimes also called the accelerated depreciation method.

If you’re brand new to the concept, open another tab and check out our complete guide to depreciation. Then come back here—you’ll have the background knowledge you need to learn about double-declining balance.

An asset for a business cost $1,750,000, will have a life of 10 years and the salvage value at the end of 10 years will be $10,000. You calculate 200% of the straight-line depreciation, or a factor of 2, and multiply that value by the book value at the beginning of the period to find the depreciation expense for that period.

- Straight-Line Depreciation Percent = 100% / 10 years = 10% / year

- Depreciation Rate = 2 x 10% = 20% / year

- Depreciation for a Period = 20% x Book Value at Beginning of the Period

- Depreciation for Period 1 = 20% x $1,750,000 = $350,000

- For Periods 2 and greater, depreciation is 20% x ($1,750,000 – Accumulated Depreciation )

- Depreciation for Period 2 = 20% x ($1,750,000 – $350,000 ) = $280,000

- Depreciation for Period 3 = 20% x ($1,750,000 – $630,000 ) = $224,000

The most basic type of depreciation is the straight line depreciation method. You use it to write off the same depreciation expense every year. So, if an asset cost $1,000, you might write off $100 every year for 10 years. Your annual depreciation amount never changes.

Double Declining Balance Depreciation

The cost of the asset is what you paid for an asset. The recovery period, or the useful life of the asset, is the period over which you’re depreciating it, in years. Once you’ve done this, you’ll have your basic yearly write-off. You can use this to get your basic depreciation rate.

Basic yearly write-off/cost of the asset The result is your basic depreciation rate expressed as a decimal. (You can multiply it by 100 to see it as a percentage.) This is also called the straight-line depreciation rate—the percentage of an asset you depreciate each year if you use the straight-line method.

Read Also: What Is Net Working Capital?

Every year you write off part of a depreciable asset using double-declining balance, you subtract the amount you wrote off from the asset’s book value on your balance sheet. Starting off, your book value will be the cost of the asset—what you paid for the asset.

That number goes down each year, as you subtract the amount you wrote off.

When accountants use double-declining appreciation, they track the accumulated depreciation—the total amount they’ve already appreciated—in their books, right beneath where the value of the asset is listed. If you’re calculating your own depreciation, you may want to do something similar and include it as a note on your balance sheet.

How do you calculate a double declining balance?

First, Divide “100%” by the number of years in the asset’s useful life, this is your straight-line depreciation rate. Then, multiply that number by 2 and that is your Double–Declining Depreciation Rate. In this method, depreciation continues until the asset value declines to its salvage value.

How does double-declining balance depreciation?

The double-declining balance method of depreciation, also known as the 200% declining balance method of depreciation, is a form of accelerated depreciation.