What Is Net Working Capital?

Net Working Capital: Net working capital (NWC) is the characteristic between a company’s current assets and current liabilities. A positive net working capital points out a company has sufficient funds to meet its current financial accountabilities and invest in other activities. For example, if current assets are $85,000 and current liabilities are $40,000, the NWC is $45,000.

Simply put, Net Working Capital (NWC) is the difference between a company’s current assets and ongoing liabilities on its balance sheet. It is a measure of a company’s liquidity and its capability to meet short-term accountabilities, as well as fund operations of the business. The ideal position is to have more current assets than current accountabilities, and thus have a positive net managing capital balance.

Net Working Capital Formula

If the net managing capital figure is substantially confident, it indicates that the short-term funds available from current wealth are more than adequate to pay for current liabilities as they come due for payment. If the figure is considered negative, then the employer may not have satisfactory funds available to pay for its current liabilities, and maybe in danger of liquidation. The networking capital figure is more instructional when tracked on a trend line, since this may show a gradual improvement or decline in the net amount of working capital over time. Networking capital can also be used to predict the ability of a corporation to grow instantaneously.

If it has substantial cash reserves, it may have suitable cash to rapidly scale up the business. Conversely, a tight working metropolis situation makes it quite unlikely that a business has the financial means to accelerate its rate of growth. A more limited indicator of the ability to grow is when accounts chargeable settlement terms are shorter than the records payable terms, which means that a company can collect cash from its customers before it needs to pay its suppliers.

The networking capital figure can be extremely misleading for the following reasons:

- Line of credit. Employment may have a large line of credit available that can easily pay for any short-term funding shortfalls indicated by the net engaged capital measurement, so there is no real risk of liquidation. Instead, the line of credit is used at any time an obligation must be paid. A more nuanced view is to plot networking capital against the remaining available balance above the line of credit.

- if the line has been approximately consumed, then there is a greater potential for a liquidity problem. Anomalies. If only measured as of one date, the measurement may include an abnormality that does not aberration the general trend of net working capital. For example, a large one-time account payable may not yet be paid, and so appears to create a negligible net working capital figure.

- Liquidity. Modern assets are not unquestionably very liquid, and so may not be available for use in paying down short-term liabilities. In exceptional, inventory may only be convertible to cash at a steep discount, if at all. Further, accounts receivable may not be collectible in the short term, principally if credit terms are excessively long. This is a particular problem when large customers have considerable bargaining power over the business, and so can voluntarily delay their payments.

What Is Net Working Capital

Networking financing is a liquidity calculation that measures a company’s ability to pay off its current liabilities with current assets. This evaluation is important to the administration, vendors, and general creditors because it shows the firm’s short-term liquidity as well as management’s ability to use its assets efficiently. Much like the working capital ratio, the net engaged capital formula focal point on current liabilities like trade debts, accounts payable, and vendor notes that must be repaid in the ongoing year.

It only makes sense the vendors and creditors would like to see how much current assets, assets that are expected to be converted into cash in the ongoing year, are available to pay for the involvements that will become due in the coming 12 months.

If a company can’t meet its current accountabilities with current assets, it will be forced to use it’s long-term assets, or income producing assets, to pay off its current understandings. This can lead to decreased surgeries, sales, and may even be an indicator of more severe organizational and financial problems.

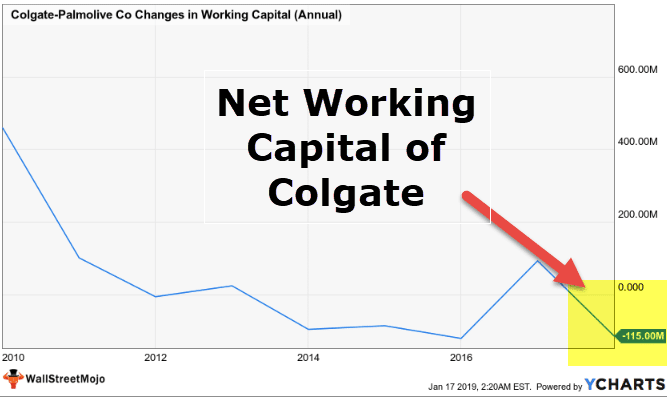

Change In Net Working Capital

Asimismo, el precio que el comprador debe pagar por el valor de las acciones “Equity Value” será igual al “Enterprise Value” que corresponde con el precio asignado al negocio del Target en la fecha de valoración, independientemente del tipo de método de valoración que utilicemos (Múltiplos, DFC, etc.), menos la Deuda Neta “Net debt” (Deuda financiera – efectivo y otros activos líquidos equivalentes).

Aunque parezca a simple vista que el NWC no es relevante en la determinación del precio, debemos decir que sí juega un papel importante debido a que sus variaciones generan entradas/salidas de caja y, por tanto, afectan a la Deuda Neta. En consecuencia, debemos establecer mecanismos de ajuste[1] que permitan proteger al comprador de variaciones “no naturales” del NWC a fecha de cierre, que pueden afectar negativamente al precio final a pagar. A continuación, se detallan una serie de ejemplos de cómo puede afectar el NWC al precio final:

- Aplicando medidas como pueden ser el retraso en el registro de facturas o de pago a proveedores, adelanto del cobro de clientes, reclasificaciones de partidas, etc., pueden incrementar la tesorería a fecha de cierre y, por tanto, el precio a pagar por el comprador.

Dependiendo de cómo las partes definan el NWC y Deuda Neta, pueden existir partidas que se consideran como Deuda Neta (los denominados “debt like ítems”) que si no se han tenido en consideración desde el principio, o bien pueden suponer un “deal break” en los momentos finales de la negociación (cuando el comprador ya ha asumido importantes gastos derivados del análisis de la transacción) o pueden suponer que, una vez se haga efectiva la toma de control del Target, se tengan que hacer una serie de pagos no previstos que se deberían haber descontado del precio. Algunos ejemplos pueden ser (facturas de proveedores vencidas o aplazadas, aplazamientos de deudas con administraciones públicas, depósitos recibidos que se deban devolver, provisiones por riesgos, indemnizaciones, etc).

Por ello, el objetivo de análisis para el NWC en una compraventa de una empresa debe permitir disponer de una imagen clara de lo que se incluye/excluye para determinar un NWC ajustado y normalizado, como base para la negociación, así como para entender las necesidades operativas de financiación presentes y futuras existentes para el comprador desde el día después de la toma el control efectiva de la empresa.

Finalmente, como resumen, se describe a continuación una forma, que no la única, de proteger al comprador frente a variaciones deliberadas del NWC que pueden incrementar el precio a fecha de cierre de la operación. Para ello se recomienda:

- Establecer una definición clara de lo que se entiende por NWC. Para lograrlo, puede ser de ayuda este otro artículo publicado en nuestro microsite sobre la importancia de la adecuada definición de las cláusulas financieras en los acuerdos de compraventa de empresas.

- Realizar un análisis sobre el NWC a la fecha de referencia para obtener un NWC ajustado con base en la definición del punto anterior.

- Determinar un NWC normalizado. No existe una fórmula establecida para su determinación, pero un método aceptado en muchos negocios es considerar un porcentaje del NWC ajustado sobre ventas acumuladas de un periodo relativamente extenso.

- Incorporación al mecanismo de ajuste de precio del ajuste al NWC. El ajuste correspondiente resultaría de comparar el NWC ajustado a la fecha de cierre con el NWC normalizado o de referencia.

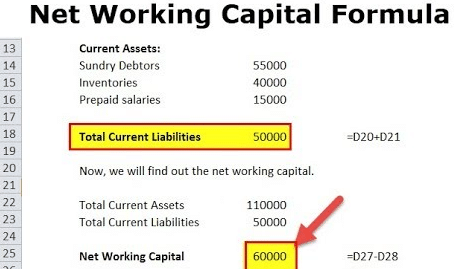

How To Calculate Net Working Capital

Working capital (abbreviated WC) is a financial metric that represents operating liquidity available to a business, organization, or other entity, including governmental entities. Along with fixed assets such as plant and equipment, working capital is considered a part of operating capital. Gross working capital is equal to current assets. Working capital is calculated as current assets minus current liabilities.[1] If current assets are less than current liabilities, an entity has a working capital deficiency, also called a working capital deficit.

A company can be endowed with assets and profitability but may fall short of liquidity if its assets cannot be readily converted into cash. Positive working capital is required to ensure that a firm is able to continue its operations and that it has sufficient funds to satisfy both maturing short-term debt and upcoming operational expenses. The management of working capital involves managing inventories, accounts receivable and payable, and cash.

In contrast, another company that sells fast-moving products online with customers paying with credit cards will have liquidity even with a small amount of net working capital. If this company’s suppliers also have credit terms of net 60 days or the company pays its bills by using its business credit card, the company may be able to operate with negative working capital.

In short, networking capital management is critical for a company’s positive relationships with lenders, suppliers, employees, and customers. All of the components of networking capital should be examined in detail and managed properly. Also Read – Times Interest Earned Ratio

How do you calculate net working capital?

Calculating Net Working Capital

Networking capital is calculated by subtracting total current liabilities from total current assets. Assets and liabilities are considered current if they are expected to be used or paid within one year. Current assets include all of the liquid assets discussed previously.