Accounting Profit | Accounting Profit Definition

Accounting profit is a company’s total earnings, calculated according to generally accepted accounting principles (GAAP). It includes the explicit costs of doing business, such as operating expenses, depreciation, interest, and taxes.

Profit is a widely monitored financial metric that is regularly used to evaluate the health of a company. Firms often publish various versions of profit in their financial statements. Some of these figures take into account all revenue and expense items, laid out in the income statement. Others are creative interpretations put together by management and their accountants.

Accounting profit also referred to as bookkeeping profit or financial profit, is net income (NI) earned after subtracting all dollar costs from total revenue. In effect, it shows the amount of money a firm has left over after deducting the explicit costs of running the business.

Accounting Profit Vs Economic Profit

Accounting Profit

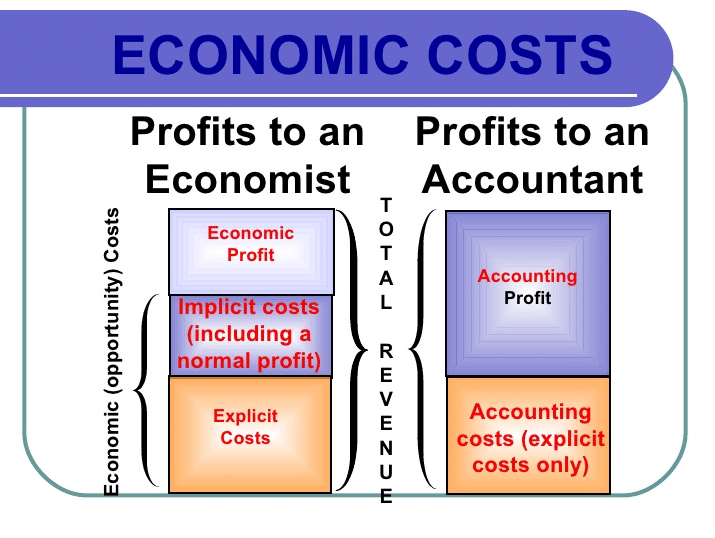

Accounting profit is the difference between total monetary revenue and total monetary costs and is computed by using generally accepted accounting principles (GAAP). Put another way, accounting profit is the same as bookkeeping costs and consists of credits and debits on a firm’s balance sheet. These consist of the explicit costs a firm has to maintain production (for example, wages, rent, and material costs). The monetary revenue is what a firm receives after selling its product in the market.

Accounting profit is also limited in its time scope; generally, accounting profit only considers the costs and revenue of a single period of time, such as a fiscal quarter or year.

Economic Profit

Economic profit is the difference between total monetary revenue and total costs, but total costs include both explicit and Implicit Costs. Economic profit includes the opportunity costs associated with production and is, therefore, lower than accounting profit. Economic profit also accounts for a longer span of time than accounting profit. Economists often consider long-term economic profit to decide if a firm should enter or exit a market.

Accounting Profit Formula

Let’s look at an example of how accounting profit is calculated. Company A operates in the manufacturing industry and sells widgets for $5. In January, it sold 2,000 widgets for total monthly revenue of $10,000. This is the first number entered into its income statement.

The cost of goods sold (COGS) is then subtracted from revenue to arrive at gross revenue. If it costs $1 to produce a widget, the company’s COGS would be $2,000, and its gross revenue would be $8,000, or ($10,000 – $2,000).

Read Also: Marginal Revenue Formula

After calculating the company’s gross revenue, all operating costs are subtracted to arrive at the company’s operating profit, or earnings before interest, taxes, depreciation, and amortization (EBITDA). If the company’s only overhead was a monthly employee expense of $5,000, its operating profit would be $3,000, or ($8,000 – $5,000).

Once a company derives its operating profit, it then assesses all non-operating expenses, such as interest, depreciation, amortization, and taxes. In this example, the company has no debt but has depreciating assets at a straight-line depreciation of $1,000 a month. It also has a corporate tax rate of 35%.

The depreciation amount is first subtracted to arrive at the company’s earnings before taxes (EBT) of $1,000, or ($2,000 – $1,000). Corporate taxes are then assessed at $350, to give the company an accounting profit of $650, calculated as ($1,000 – ($1,000 * 0.35).

Accounting Profit vs. Underlying Profit

Companies often choose to supplement accounting profit with their own subjective take on their profit position. One such example is the underlying profit. This popular, widely-used metric often excludes one-time charges or infrequent occurrences and is regularly flagged by management as a key number for investors to pay attention to.

The goal of underlying profit is to eliminate the impact that random events, such as a natural disaster, have on earnings. Losses or gains that do not regularly crop up, such as restructuring charges or the buying or selling of land or property, are usually not taken into account because they do not occur often and, as a result, are not deemed to reflect the everyday costs of running the business.

Non Profit Accounting

From churches to youth organizations to the local chambers of commerce, nonprofit organizations make our communities more livable places. Unlike for-profit businesses that exist to generate profits for their owners, nonprofit organizations exist to pursue missions that address the needs of society. Nonprofit organizations serve in a variety of sectors, such as religious, education, health, social services, commerce, amateur sports clubs, and the arts.

Nonprofits do not have commercial owners and must rely on funds from contributions, membership dues, program revenues, fundraising events, public and private grants, and investment income.

Our intent is to merely introduce some of the basic concepts that are unique to nonprofit accounting and reporting that are required by the Financial Accounting Standards Board (FASB).

We will not discuss the accounting that is similar to that used by for-profit businesses. If you are not familiar with accounting for businesses or you wish to refresh your understanding, you will find free explanations, quizzes, Q&A, and more at Accounting Topics.

Accountants often refer to businesses as for-profit entities and to nonprofit organizations as not-for-profit entities or NFPs. We will be using the more common term nonprofit instead of not-for-profit.

What Is Accounting Profit?

This is the net income reported on all GAAP basis financial statements. Accountants subtract a firm’s explicit costs from the total revenues to calculate the accounting profit. Explicit costs are costs that can be clearly identified and measured. For example, labor costs are explicit costs because they represent a specific amount paid for wages during a given period.

All of the costs included in the calculation are amounts actually paid except depreciation expense. This represents the year’s ratable portion of the past outlay of cash required to purchase production equipment. Thus, this also is included.

Accountants do not consider implicit costs in this calculation because they haven’t been incurred and are merely theoretical. Implicit costs are used for the calculation of a firm’s economic profit.

How To Calculate Accounting Profit

Let’s look at an example.

Example

Mario, the chief accountant of a manufacturing company that sells air conditioners, asks his assistant to calculate the firm’s accounting profit over the past three years. Mario wants to confirm that the profit of the company is increasing, indicating that the company is effectively managing its costs.

The assistant creates an excel file with all the information he has for the firm’s operations in 2013, 2014, and 2015, i.e. total revenues and explicit costs (rent, mortgage, wages, raw materials, and electricity expenses).

The assistant finds that the profit for the company in the fiscal year 2015 is $2.27 million, for 2014 is $2.09 million and for 2013 is $1.96 million. The increase of 8.47% YoY from 2014 to 2015 and of 6.81% YoY from 2013 to 2014 indicates that the firm implements effective strategies to lower its explicit costs and increase its revenues. Specifically, the revenue growth from 2013 to 2014 is 5.60% YoY and from 2014 to 2015 is 8.33% YoY.

Furthermore, the company has lowered its raw materials costs by 4.35% YoY from 2013 to 2014, and by 3.03% YoY from 2014 to 2015. Likewise, the electricity costs are reduced by 3.53% YoY from 2013 to 2014 and by 3.53% YoY from 2014 to 2015.