Retained Earnings Formula

Retained earnings Formula (REF) is the amount of net income left over for the business after it has paid out dividends to its shareholders. A business generates earnings that can be positive (profits) or negative (losses).

Positive profits give a lot of room to the business owner(s) of the Company Management to utilize the surplus money earned. Often this profit is paid out to shareholders, but it can also be reinvested back into the company for growth purposes. The money not paid to shareholders counts as retained earnings.

Retained earnings represent a useful link between the income statement and the balance sheet, as they are recorded under shareholders’ equity which connects the two statements. The purpose of retaining these earnings can be varied and includes buying new equipment and machines, spending on research and development, or other activities that could potentially generate growth for the company. This reinvestment into the company aims to achieve even more earnings in the future.

If a company does not believe it can earn a sufficient return on investment from those retained earnings (i.e., earn more than their cost of capital) then they will often distribute those earnings to shareholders as dividends or share buybacks.

Formula For Retained Earnings

Retained Earnings (RE) are the portion of a business’s profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. Normally, these funds are used for working capital and fixed asset purchases (capital expenditures) or allotted for paying off debt obligations.

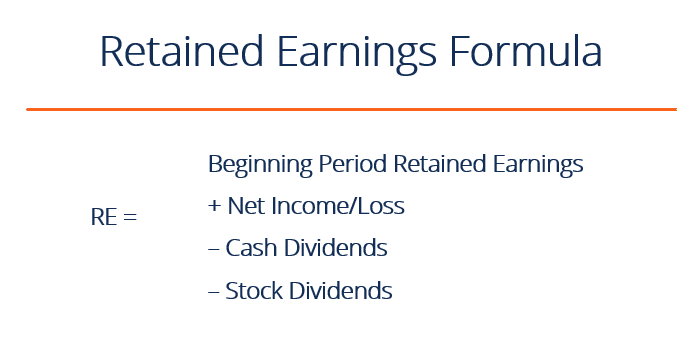

The RE formula is as follows:

RE = Beginning Period RE + Net Income/Loss – Cash Dividends – Stock Dividends

Where RE = Retained Earnings

Ending Retained Earnings Formula

Addition-To Retained Earnings Formula

Whenever a company generates surplus income, a portion of the long-term shareholders may expect some regular income in the form of dividends as a reward for putting their money in the company. Traders who look for short-term gains may also prefer getting dividend payments that offer instant gains.

Dividends are also preferred as many jurisdictions allow dividends as tax-free income, while gains on stocks are subject to taxes. On the other hand, company management may believe that they can better utilize the money if it is retained within the company. Similarly, there may be shareholders who trust the management potential and may prefer allowing them to retain the earnings in hopes of much higher returns (even with the taxes).

KEY TAKEAWAYS

- Retained earnings (RE) is the amount of net income left over for the business after it has paid out dividends to its shareholders.

- The decision to retain the earnings or to distribute it among the shareholders is usually left to the company management.

- A growth-focused company may not pay dividends at all or pay very small amounts, as it may prefer to use the retained earnings to finance expansion activities.

Statement Of Retained Earnings Formula

The following options broadly cover all possibilities on how the surplus money can be utilized:

- The income money can be distributed (fully or partially) among the business owners (shareholders) in the form of dividends.

- It can be invested to expand the existing business operations, like increasing the production capacity of the existing products or hiring more sales representatives.

- It can be invested to launch a new product/variant, like a refrigerator maker foraying into producing air conditioners, or a chocolate cookie manufacturer launching orange- or pineapple-flavored variants.

- The money can be utilized for any possible merger, acquisition, or partnership that leads to improved business prospects.

- It can also be used for share buybacks.

- The earnings can be used to repay any outstanding loan (debt) the business may have.

The first option leads to the earnings money going out of the books and accounts of the business forever because dividend payments are irreversible. However, all the other options retain the earnings money for use within the business, and such investments and funding activities constitute the retained earnings (RE).

By definition, retained earnings are the cumulative net earnings or profits of a company after accounting for dividend payments. It is also called earnings surplus and represents the reserve money, which is available to the company management for reinvesting back into the business. When expressed as a percentage of total earnings, it is also called retention ratio and is equal to (1 – dividend payout ratio).

While the last option of debt repayment also leads to the money going out, it still has an impact on the business accounts, like saving future interest payments, which qualifies it for inclusion in retained earnings.

Calculate Retained Earnings Formula

The decision to retain the earnings or to distribute it among the shareholders is usually left to the company management. However, it can be challenged by the shareholders through the majority vote as they are the real owners of the company.

Management and shareholders may like the company to retain the earnings for several different reasons. Being better informed about the market and the company’s business, the management may have a high growth project in view, which they may perceive as a candidate to generate substantial returns in the future. In the long run, such initiatives may lead to better returns for the company shareholders instead of that gained from dividend payouts. Paying off high-interest debt is also preferred by both management and shareholders, instead of dividend payments.

Read Also: Marginal Revenue Formula

Most often, a balanced approach is taken by the company’s management. It involves paying out a nominal amount of divide and retaining a good portion of the earnings, which offers a win-win.

Retained Earnings Formula Accounting

Any changes or movement with net income will directly impact the RE balance. Factors such as an increase or decrease in net income and incurrence of net loss will pave the way to either business profitability or deficit. The Retained Earnings account can be negative due to large, cumulative net losses. Naturally, the same items that affect net income effect RE.

Examples of these items include sales revenue, cost of goods sold, depreciation, and other operating expenses. Non-cash items such as write-downs or impairments and stock-based compensation also affect the account.

How To Find Retained Earnings Formula

RE=BP+Net Income (or Loss)−C−where: BP=Beginning Period REC=Cash dividendsS=Stock dividends

Beginning Retained Earnings Formula

At the end of each accounting period, retained earnings are reported on the balance sheet as the accumulated income from the prior year (including the current year’s income), minus dividends paid to shareholders. In the next accounting cycle, the RE ending balance from the previous accounting period will now become the retained earnings beginning balance.

The RE balance may not always be a positive number as it may reflect that the current period’s net loss is greater than that of the RE beginning balance. Alternatively, a large distribution of dividends that exceed the retained earnings balance can cause it to go negative.